This section contains an non-exhaustive overview of national policies outside the EU that promote the use of SAF.

Switzerland set out a SAF strategy with the goal that SAF shall contribute a minimum of 60% to net CO2 reductions in Swiss civil aviation by 2050, thereby contributing to the Swiss goal of reaching net-zero CO2 emissions in 2050. It is accompanied by a legislative proposal that includes a blending mandate and provision of funding for the development of SAF production pathways, planned to enter into force in 2025. To avoid market distortion, the mandate shall be aligned with ReFuelEU Aviation. Turkey is also planning to develop dedicated SAF regulations to incentivize its uptake

[24]

. The United Kingdom SAF policy includes a SAF Mandate to drive an ambitious ramp-up of SAF in the aviation fuel supply, starting with 2% in 2025, increasing linearly to 10% in 2030 and reaching 22% in 2040. The Mandate includes a cap on the amount of HEFA SAF used to meet obligations, and there is a separate obligation for Power-to-Liquid fuels, starting in 2028 with 0.2% of the total fuel supply and reaching 3.5% in 2040

[25]

.

Outside of Europe, the United States has introduced the ‘SAF Grand Challenge’ to produce at least 3 billion gallons (approx. 94 million tonnes) per year by 2030

[26]

. This is being incentivized by tax credits for producers and a grant program to boost domestic SAF production. Both South Korea and Indonesia plan to have all departing international flights use a mix of 1% SAF from 2027, with Indonesia planning to ramp up this mandate from 2.5% in 2023 up to 50% in 2060

[27]

[28]

. Singapore aims at a 1% SAF target for all departing flights from 2026 that will increase to 3-5% by 2030, and which is supported by the introduction of a levy for the purchase of SAF

[29]

. The Japanese Ministry of Trade and Industry has set a 10% SAF blending target on domestic airlines fuel consumption by 2030 that includes support to develop new technologies to produce SAF

[30]

.

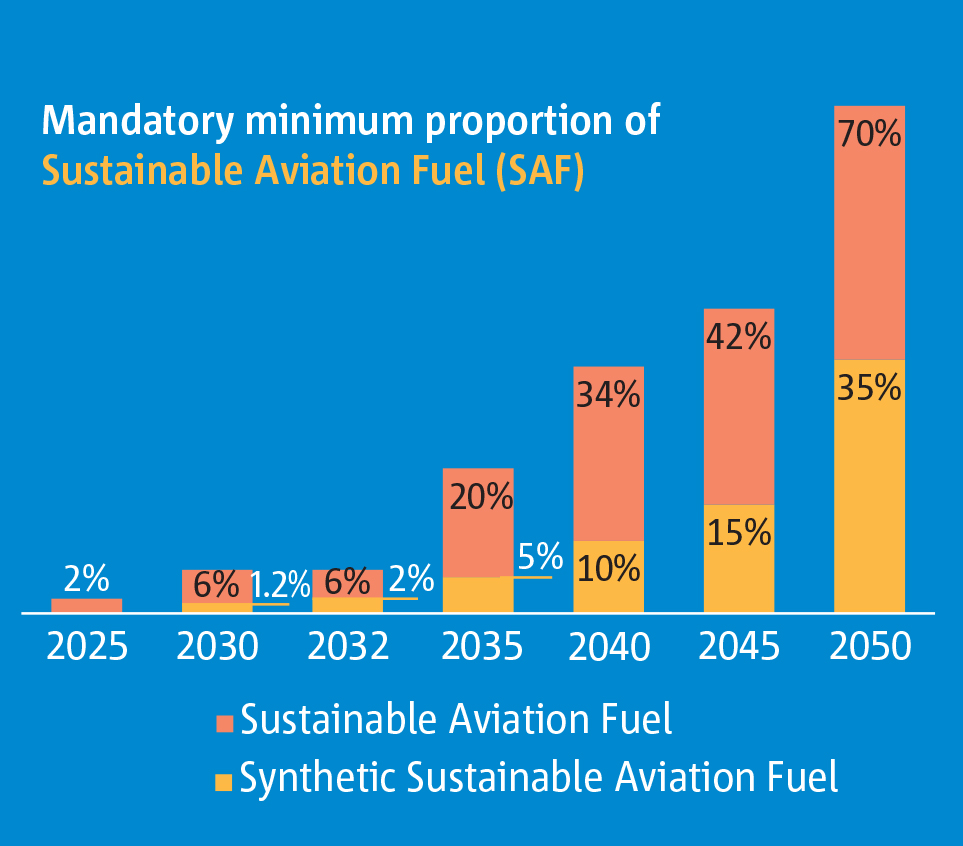

The ReFuelEU Aviation Regulation sets out EU-level harmonised obligations on aviation fuel suppliers, aircraft operators and Union airports for scaling up SAF used for flights departing from all EU airports above certain annual traffic thresholds (passenger traffic above 800 000 or freight traffic above 100 000 tons). Starting in 2025, aviation fuel suppliers are required to supply a minimum of 2% blend of SAF with conventional aviation fuels to Union airports and this gradually increases to at least 70% by 2050. Synthetic aviation fuels are subject to a dedicated minimum share, starting with 1.2% in 2030, 2% in 2032 and reaching 35% in 2050

The ReFuelEU Aviation Regulation sets out EU-level harmonised obligations on aviation fuel suppliers, aircraft operators and Union airports for scaling up SAF used for flights departing from all EU airports above certain annual traffic thresholds (passenger traffic above 800 000 or freight traffic above 100 000 tons). Starting in 2025, aviation fuel suppliers are required to supply a minimum of 2% blend of SAF with conventional aviation fuels to Union airports and this gradually increases to at least 70% by 2050. Synthetic aviation fuels are subject to a dedicated minimum share, starting with 1.2% in 2030, 2% in 2032 and reaching 35% in 2050  The third ICAO Conference on Aviation Alternative Fuels (CAAF/3) was held in November 2023, during which ICAO Member States agreed on the ICAO Global Framework for SAF, Lower Carbon Aviaton Fuels (LCAF) and other Aviation Cleaner Energies. This includes a collective global aspirational vision to reduce CO2 emissions from international aviation by 5% in 2030 with the increased production of SAF, LCAF and other initiatives [23]. Building blocks in terms of policy and planning, regulatory framework, implementation support and financing will be key in achieving this goal. The vision will be continually monitored and periodically reviewed, including through the convening of CAAF/4 no later than 2028, with a view to updating the ambition on the basis of market developments in all regions.

The third ICAO Conference on Aviation Alternative Fuels (CAAF/3) was held in November 2023, during which ICAO Member States agreed on the ICAO Global Framework for SAF, Lower Carbon Aviaton Fuels (LCAF) and other Aviation Cleaner Energies. This includes a collective global aspirational vision to reduce CO2 emissions from international aviation by 5% in 2030 with the increased production of SAF, LCAF and other initiatives [23]. Building blocks in terms of policy and planning, regulatory framework, implementation support and financing will be key in achieving this goal. The vision will be continually monitored and periodically reviewed, including through the convening of CAAF/4 no later than 2028, with a view to updating the ambition on the basis of market developments in all regions.